An airline that offers you to pay for your plane ticket in several installments, a real estate agency that helps you obtain a loan… these are some of the new services introduced by open banking. Forced to open their data to new players and in competition with fintechs, banks are trying to maintain control. Their weapons? Turnkey services that can be used by any company via BaaS (Bank as a Service) platforms. In this second part on open banking, Dominique Chesneau, finance specialist and ORSYS trainer, dissects the ins and outs of this revolution.

As We have seen it, the European PSD2 directive forced banks to open access to their customers' data to third parties, such as fintechs. Result: banking services for consumers have experienced a real boom.

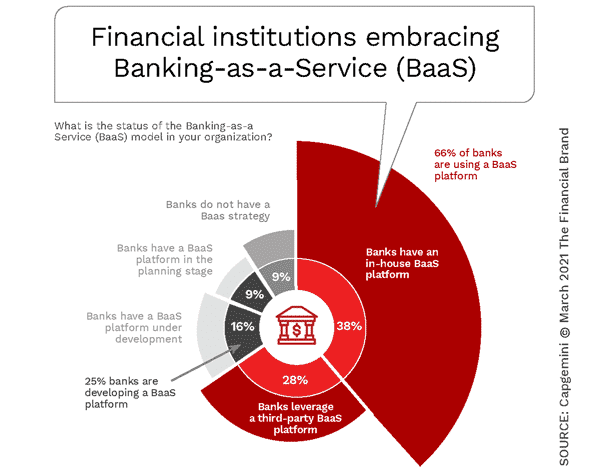

The boom in banking services via Bank as a Service (BaaS)

For many banks, open banking amounts to setting up a platform of “ Bank as a Service » (BaaS).

Inspired by “ Software as a Service » (SaaS) from software publishers, BaaS consists of offering banking services via banking APIs, interfaces allowing various operators to share information.

Concretely, a bank will not only be able to advise its customers on a real estate loan, but also help them in their real estate search in conjunction with a partner specializing in the field, such as a network of real estate agencies.

BaaS allows data to be accessed and processed remotely using, where applicable, the bank's software and information supports. It also contributes to strengthening and improving the distribution of “in-house” banking products, to reducing and automating the back office in order to increase customer satisfaction and therefore retention while reducing acquisition costs.

Some banks take advantage of a differentiation on which their legitimacy is not discussed in areas relating to consumer protection, data security, transparency, confidentiality of exchanges, etc.

This situation requires a new approach to relationships with customers, partners and competitors. It is a reflection on internal behavior in terms of creativity, responsiveness, cross-functional relationships, productivity, the search for margins linked to the value produced rather than to the reduction of unit costs.

The graph below illustrates the share of banks having implemented BaaS (38 %), those having decided to cooperate with fintechs to join a shared BaaS platform (28 %) and those which are continuing their reflections.

The API war: BaaS versus DSP2

Unlike the APIs promoted by the PSD2 directive, banks' premium APIs are accessible directly by companies or by third parties who, in turn, provide services to companies. API developers who offer these interfaces must decide whether they are building them for direct access or for third parties.

Another decision to make is whether to simply create your own API, or to collaborate and participate in the creation of standards with other developers.

API providers can adopt a stance of independence that allows for faster development with greater control over functionality and to use APIs as a differentiation tool. This approach is already represented on the market by the premium APIs offered by banks which go beyond the requirements of the PSD2 directive.

Alternatively, API providers may choose to collaborate to lower development costs, achieve critical mass (in usage and traction), and converge on customer needs.

The APIs that result from the latter approach bring standardization, scale, and scope, and while they are also difficult to set up, they are extremely powerful once they are up and running. Collaborative API frameworks are typically defined by schemas, that is, by a group of actors coming together to solve a collective challenge.

As many enterprise customers are multinationals, enterprise APIs should be considered a global phenomenon. Therefore, the necessary standardization faces the challenge of being too strict, as it may overlook local particularities, such as different reporting and accounting requirements, single payment methods and varying expectations for user experience.

This standardization is gradually being implemented through back and forth between regulators and operators. DSP 2 opened Pandora's box, according to the French Banking Federation. The rationalization and sustainability of the sector will lead to putting back into it what the players do not have control over!

Our best training courses on the subject

- Open Banking, issues and prospects

- Fintech and Big Tech in finance, state of the art and trends

- Open data, the main principles, preparing your approach to open data

data - Open innovation

- Blockchain in finance: understanding Bitcoin and cryptocurrencies